The $500M mistake your bank ‘prevented’ with this one control (and why it almost failed).

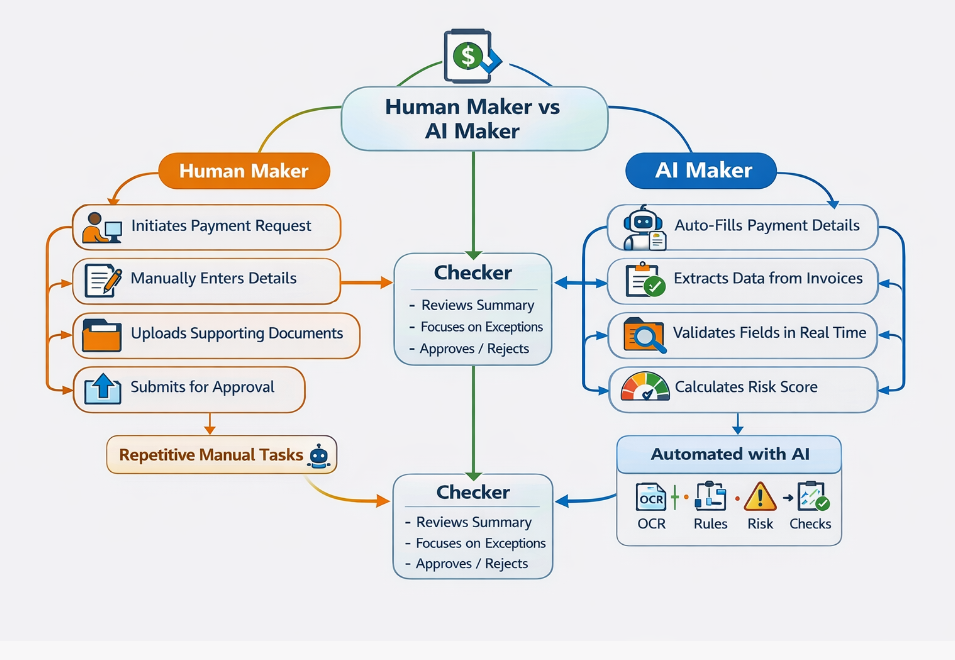

What if your riskiest financial transactions were approved by a single human. That’s where the ‘Maker-Checker ‘ principle comes in – a vital control in risk management and data governance, often called the ‘Four-Eye Principle.’

At its core, it ensures that for any sensitive task, two people are involved one to initiate (the Maker) and one to verify and authorize (the Checker). This prevents errors and fraud. Historically, this has been a manual, labor-intensive process, especially in banking’s internal operations.

Now, imagine the Maker being AI, and the Checker remaining human.

This isn’t just a futuristic concept; it’s becoming a regulatory and operational necessity, especially in high-stakes areas like AML, KYC, Payment Transactions, and Tax where precision and

compliance are paramount. As organizations navigate complex, country-specific regulations, the question shifts: How can we confidently integrate AI into the ‘Maker’ role to enhance security and efficiency, without compromising human oversight?

What are the biggest challenges you foresee in this evolution?

We talk a lot about ‘maker-checker’ in payments, but do you know where it REALLY applies? And more importantly, what happens when it breaks? Here’s a deep dive into this crucial but often misunderstood safeguard:

**Common regulated maker-checker use cases:**

1. Payment initiation:

– Maker creates a payment (wire, bulk file).

– Checker rigorously verifies: Amount, Beneficiary, Purpose, Limits & Sanctions. This isn’t just ticking a box; it’s a second pair of eyes preventing catastrophic errors.

2. Changes to standing data: This is where things get truly risky. Think:

– Beneficiary account details (redirecting funds).

– Payment templates (baking errors into future transactions).

– Settlement instructions, Bank master data.

3. Limit and permission changes:

– User access rights, Transaction limits, Approval thresholds. These are the keys to the kingdom.

4. Exception handling:

– Overrides of failed/flagged payments, Manual repairs. These are the moments when a robust maker-checker saves the day – or reveals systemic weaknesses.

The Non-Negotiables: Regulatory Expectations (Across EBA, FCA, MAS, RBI, FFIEC):

Independence: Checker must be a different individual, ideally in a different role or team. No self-approvals.

Competence: The checker *must* understand what they’re approving. Rubber-stamping is not checking.

Audit trail: Systems *must* log: Who, What, When, and all changes.

Proportionality: Higher risk = Stronger checks.

No shared credentials: Shared logins obliterate maker-checker. It’s a common, unforgivable regulatory finding.

What makes a control Strong vs. Weak?

Strong control:

– Different users, unique credentials

– Independent, diligent review

– System-enforced separation (can’t bypass)

– Clear approval thresholds, rigorously applied

– Evidence retained for audit

Weak control (regulatory red flags):

– Same person acts as maker and checker

– Auto-approvals (aka ‘fake’ checking)

– Manual controls with no audit trail

– ‘Temporary’ overrides that become permanent policy

How Regulators Uncover Failures:

They’ll ask: Can one person move funds end-to-end? What prevents self-approval? Are emergency overrides logged? How do you enforce segregation in small teams?

Failure here isn’t minor; it’s cited under:

– Internal controls weaknesses

– Operational risk deficiencies

– Governance and risk management issues

One important nuance, often missed:

Maker-checker is *necessary* but not *sufficient*.

Regulators expect it to work alongside:

– Transaction monitoring

– Limits and thresholds

– Reconciliations

– Access reviews

– Independent audits

Think of it as the foundational brick, not the entire payment fortress. Overlook it, and your entire system is vulnerable. What if your riskiest financial transactions were approved by a single human? That’s where the ‘Maker-Checker ‘ principle com es in – a vital control in risk management and data governance, often called the ‘Four-Eye Principle.’

At its core, it ensures that for any sensitive task, two people are involved one to initiate (the Maker) and one to verify and authorize (the Checker). This prevents errors and fraud. Historically, this has been a manual, labor-intensive process, especially in banking’s internal operations.

Now, imagine the Maker being AI, and the Checker remaining human. This isn’t just a futuristic concept; it’s becoming a regulatory and operational necessity, especially in high-stakes areas like AML, KYC, Payment Transactions, and Tax where precision and compliance are paramount. As organizations navigate complex,

country-specific regulations, the question shifts: How can we confidently integrate AI into the ‘Maker’ role to enhance security and efficiency, without compromising human oversight?

What’s the biggest maker-checker challenge you’ve encountered in your control testing?