Why RCSA (Risk Self-Control Assessment) isn’t just theory. It’s the one process that lets banks see danger coming (and fix it) –before– it hits.

It’s where business units identify their –own– risks, evaluate their –own– controls, and –own– their risk posture.

Here’s why it’s not just another audit process:

Proactive: Spotting problems –before– they become $5M headaches.

Empowering: Puts risk ownership directly in the hands of the business.

Dynamic: Adapts continuously, unlike static annual reviews.

In simple terms: –RCSA answers the urgent question: “What can go wrong here, and are –we– truly controlling it well enough?”– ## Why Most Banks Still Get RCSA Wrong (and Why it Matters More Than Ever) Payments and financial services are a minefield: — Massive transaction volumes — Errors that lead to embarrassing headlines — Regulators always watching

RCSA should be your shield. It helps you: — Pinpoint blind spots: operational, tech, fraud, compliance risks. — Validate your safety nets: assessing control effectiveness. — Reduce reliance on reactive audits. — –Crucially:– Strengthen risk ownership across first line teams (this is where the real power is).

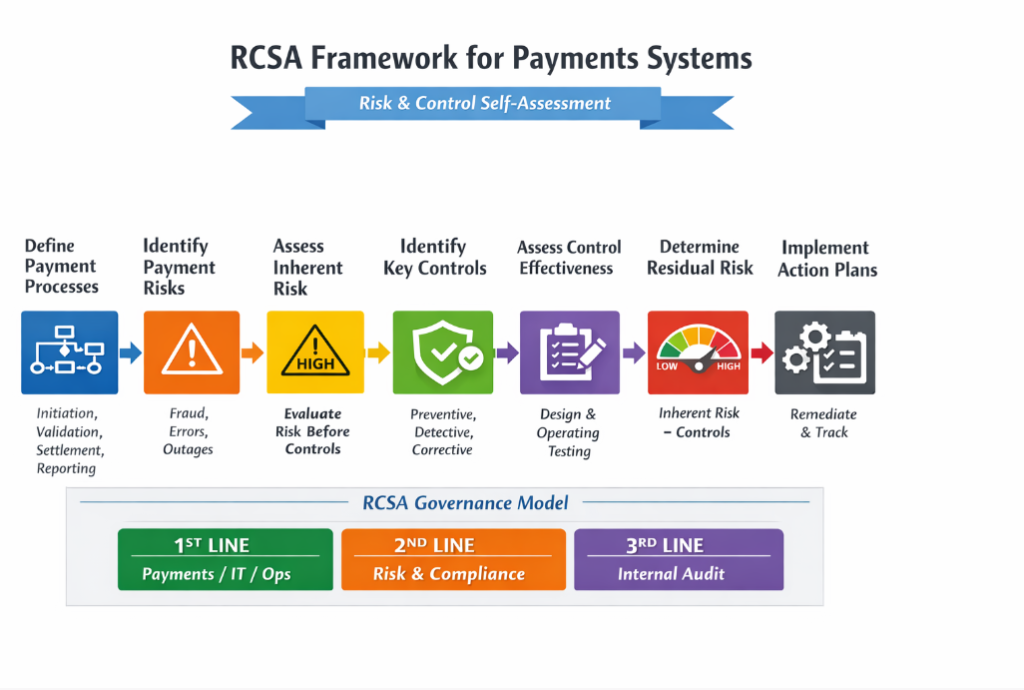

But here’s what most definitions miss: RCSA isn’t about identifying –more– risks, it’s about shifting risk –accountability– from compliance to the front lines. And that’s where most programs fail. The 6 Steps to Actual Risk Self-Control (Not Just a Checklist)

1. Risk Identification: What’s the worst that could happen? For payments, think unauthorized processing, settlement failures, data breaches. –Don’t just list — envision the impact.

2. Inherent Risk: Before any controls, how bad is it? We measure Impact (financial, reputational) vs. Likelihood (how often?). This gives you your baseline: Low / Medium / High.

3. Control Identification: What safety nets do you have? Maker-Checker approvals, role-based access, transaction limits, automated reconciliation. –Are these just ‘paper controls’ or truly embedded?–

4. Control Effectiveness: This is where the rubber meets the road. — Design Effectiveness (DE): Is your control –designed– to work? — Operating Effectiveness (OE): Is it –actually– working, consistently, day-in, day-out?

5. Residual Risk: The ultimate question: After all your controls, how much risk is –left–? This guides your actions. Is it within appetite? Or is it a red flag for senior leadership?

6. Action Plans & Remediation: If residual risk is too high, you must act. Define corrective actions, assign clear ownership, set timelines, and track progress religiously. Best Practices for RCSA Remediation Tracking – Keep the tracker live and updated—weekly reviews are ideal. – Assign clear ownership for every action. – Include evidence of closure once actions are complete. – Integrate tracker updates into risk dashboards and audit reporting. Highlight high residual risk items to senior management. What’s the biggest challenge your organization faces in truly embedding risk ownership in the first line , second line and third line ?