What is ACH = Automated Clearing House for an electronic network in the united states moves your money between bank accounts. This is payment system used to by banks and credit unions to process transfers process in batch mode it operated and monitored by : Natcha & Federal Reserve Bank.

What about other countries :

In India – NEFT (National Electronic Funds Transfer) , ECS (Electronic Clearing Services ) and NACH…

This is operated and monitored by Reserve Bank of India and National Payments Corporation of India.

APAC Regions

| Country | ACH-Type Payment | Operated By | Typical Settlement |

|---|---|---|---|

| Australia | BECS | Australian Payments Network | T+1 |

| New Zealand | Direct Credit / Direct Debit | Payments NZ | T+0–T+1 |

| Singapore | GIRO | Association of Banks in Singapore | T+1–T+2 |

| Malaysia | IBG | PayNet | Same day or T+1 |

| Thailand | BAHTNET* | Bank of Thailand | T+0 (RTGS for high value) |

| Indonesia | SKNBI | Bank Indonesia | Same day or T+1 |

| Philippines | PESONet | Philippine Payments Management, Inc. | Same day (batch windows) |

| Vietnam | Interbank Electronic Payment System | State Bank of Vietnam | T+0–T+1 |

| India | NACH / NEFT | National Payments Corporation of India | Same day (hourly batches) |

| Pakistan | IBFT / Clearing | State Bank of Pakistan | Same day |

| Bangladesh | BEFTN | Bangladesh Bank | T+0–T+1 |

| Sri Lanka | SLACH | Central Bank of Sri Lanka | T+1 |

| South Korea | Giro | Korea Financial Telecommunications and Clearings Institute | Same day |

| Japan | Zengin System | Japanese Bankers Association | Same day |

| China | CNAPS | People’s Bank of China | Same day (cut-off based) |

| Hong Kong | Autopay / CHATS | Hong Kong Monetary Authority | T+0 |

| Taiwan | ACH | Central Bank of the Republic of China (Taiwan) | T+1 |

European Union – SEPA (Single Euro Payments Area) and monitored and operated by European Payments Council and covers

SEPA includes:

-

All 27 countries of the European Union

-

4 EFTA countries (Iceland, Liechtenstein, Norway, Switzerland)

-

The United Kingdom

-

Andorra, Monaco, San Marino, and Vatican City

| Country / Region | ACH-Type Payment | Operated By | Typical Settlement |

|---|---|---|---|

| SEPA Zone | SEPA Credit Transfer | European Payments Council | T+1 (D+1 standard) |

| United Kingdom | BACS | Pay.UK | T+2 to T+3 |

| Switzerland | SIC | Swiss National Bank | Same day |

| Norway | NICS | Norges Bank | Same day |

| Sweden | Bankgirot | Bankgirot | Same day |

| Denmark | Sumclearing | Danmarks Nationalbank | Same day |

| Poland | ELIXIR | KIR | Same day (3 batch windows) |

| Czech Republic | CERTIS | Czech National Bank | Same day |

| Hungary | InterGIRO | Magyar Nemzeti Bank | Same day |

Middle East Countries

| Country | Domestic ACH / Bank Transfer System | Typical Settlement (T+N) |

|---|---|---|

| United Arab Emirates | UAEFTS (UAE Funds Transfer System) | T+0–T+1 |

| Saudi Arabia | SARIE (Saudi Arabian Riyal Interbank Express) | T+0–T+1 |

| Qatar | Qatar ACH (Central Bank of Qatar) | T+1–T+2 |

| Kuwait | K-Net / Interbank Transfer System | T+1 |

| Bahrain | BENEFIT (Bahrain Electronic Network for Financial Transactions) | T+0–T+1 |

| Oman | Oman ACH (Central Bank of Oman) | T+1–T+2 |

| Jordan | JOD ACH (Central Bank of Jordan) | T+1–T+2 |

| Egypt | Egypt ACH (Central Bank of Egypt) | T+0–T+1 |

| Lebanon | Lebanese Interbank ACH | T+1+ |

| Israel | ZAHAV / MASAV ACH (Bank of Israel) | T+0–T+1 |

| Turkey | EFT / ACH (Central Bank of Turkey) | T+1–T+2 |

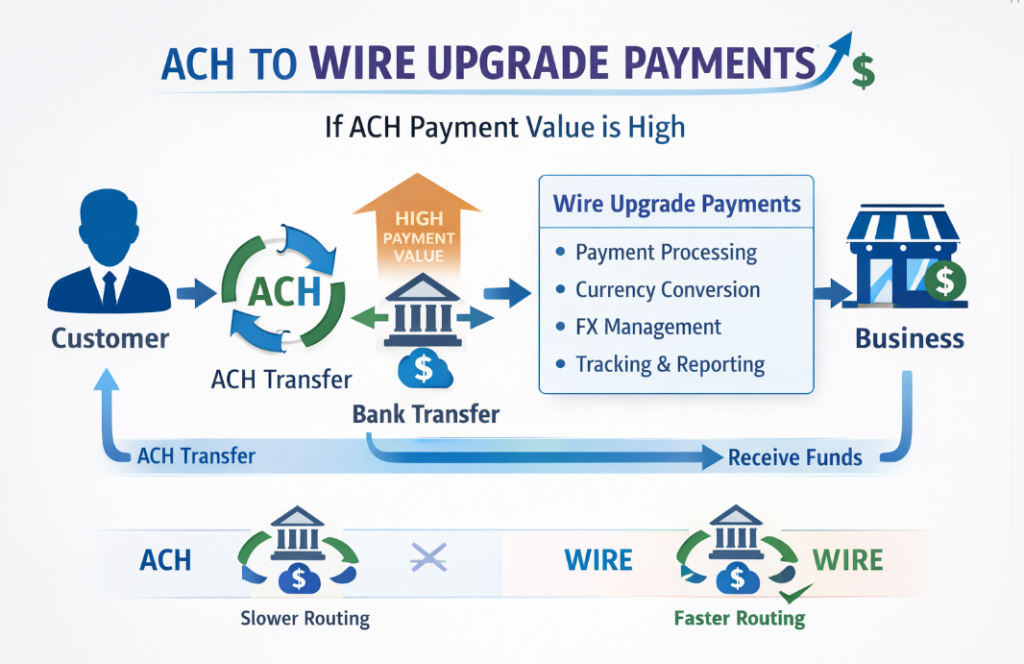

BDD Scenario

Scenario: Payment amount exceeds ACH limit

-

Given customer initiates ACH payment

-

And amount > configured ACH threshold (e.g. $100,000)

-

When payment is validated

-

Then system auto-flags payment for Wire upgrade

-

And ACH instruction is not sent downstream

-

And Wire instruction is created

Scenario: ACH message converted to Wire format

-

Given original ACH payment details

-

When upgrade occurs

-

Then Wire message (Fedwire / SWIFT MT/MX) is created

-

And beneficiary details remain unchanged

-

And payment reference is preserved

-

And original ACH trace ID is linked for audit

Scenario: Wire submission failure

-

Given ACH upgraded to Wire

-

When Wire fails (network / validation error)

-

Then:

-

Payment is not re-sent as ACH automatically

-

Customer is notified

-

Funds are held or reversed per policy

-

-

And exception workflow is triggered

Scenario: Regulatory and Compliance Scenario

-

Given payment is upgraded

-

When audit report is generated ay the maker and checker

-

Then report shows:

-

Original ACH request

-

Upgrade decision reason

-

Wire reference number

-

Timestamp & user/system ID

-

-

And complies with SOX / FFIEC requirements

Scenario: End-to-end tracking continuity for tracking the status

-

Given payment upgraded after cut off time

-

When status updates are generated

-

Then:

-

Original ACH status marked as “Upgraded to Wire”

-

Wire status progresses (Initiated → Sent → Pending → Settled/ Completed)

-

-

And customer can track payment in real time